An Omnichannel Approach to Retail Planning

Almost every week, we hear about a brand restructuring its retail store network. Most are downsizing, or rightsizing, their physical store estates, but some are seeking to open stores. It is representative of the considerable changes occurring across the retail landscape today, particularly in relation to the location of retail assets.

Recently, for example, Carpetright, the UK floor covering chain, announced restructuring plans after closing 80 of its stores in the UK and announcing that it will close some stores in Ireland, too. This isn’t uncommon as retailers respond to changing consumer habits, needs and expectations.

Consumers are choosing retail parks and easy access shopping centres over the high street, while online and ‘click and collect’ options have created a consumer that demands easy access to parking, loading, checkout and returns. As a result, once-stable retail giants are struggling to repurpose their networks to compete with the nimble online or pure-play retailers.

The retail rightsizing challenge

However, by redesigning their distribution networks – to optimise physical and online stores, as well as click and collect services – retailers can position themselves as the most convenient choice for their target market, while also restoring sustainable margins through each channel. This isn’t a channel-specific challenge, but rather a multi-layered and integrated puzzle that will be solved by identifying the most competitive, customer-centric combination of stores, delivery services and click and collect options.

For Carpetright, it’s not a simple case of closing the worst-performing stores as each store closure has an impact on the retailer’s surrounding stores. So, while closing several in an area may boost the footfall to another, closing too many could terminally affect the store’s brand strength. Research shows, somewhat counter-intuitively, that online sales for many retailers are highest closest to their physical store locations. Clearly, showrooming matters.

The online sales uplift generated by having a store in an area must therefore be factored in before evaluating the net cost of a store closure. By mapping out online and loyalty customers and their spending patterns, through location intelligence analysis, a retailer can gain a strong understanding of how their customers regard the availability of physical stores in an area. This can be measured, along with their stores’ impact on online sales. So, in closing Store X, a retailer may save €1M per year in operation costs, but the net effect may be a €2M decline in profits when online sales losses are factored in.

So, how can a retailer optimise its estate to offer a cost-effective presence that will satisfy consumer demands into the next decade? Firstly, it needs to understand its market, map it out and see how customers are engaging through each channel. The retailer needs to see where its customers are, at what times, and overlay this information with its interaction points (or stores, as we once called them!). Once this is achieved, the retailer can model and score its brand convenience in every neighbourhood. Using these insights, an optimum network that satisfies the retailer’s convenience goals can be built.

Gartner calls this new analytical requirement “omnichannel location analysis” as multi-branch retailers globally look to make informed decisions on the redistribution and reformatting of their assets in order to survive and thrive. To optimise, we must measure and enhance omnichannel convenience for the retailer’s target market, while still satisfying the retailer’s other site and market constraints.

Measuring network convenience

Convenience is the degree of friction or hassle that a consumer has to endure in order to purchase a product from a retailer. While it may seem like a vague concept to measure, this hassle can, in fact, be broken down. For physical stores, we look at friction factors: the time or difficulty it takes to travel to the store, plus the time it takes to park and enter the store, along with the time it takes to find the required products and check out. To complete the brand’s convenience score, we must also consider the friction involved in buying online – to include ease, speed of ordering, returns policies and delivery times – and, if applicable, the click and collect shopping process (ease of collections, parking and online ordering).

Scoring and valuing these criteria for a target neighbourhood will determine how convenient a retail brand is to that neighbourhood or workplace. For example, in Neighbourhood A, it takes 15 minutes to drive to the nearest Brand X store. Parking will take another five minutes and the checkout process is slow, which adds an additional 10 minutes. From the customer’s point of view, that’s 45 minutes of hassle. We can similarly assess the neighbourhood in terms of online shopping and click and collect.

Using this approach, we can score every neighbourhood in terms of its omnichannel convenience to a brand or retail chain. It requires specialist analysis and a lot of data, but even a limited, consistent approach using the data that is available can offer a good KPI to measure convenience geographically. This will reveal where your network needs to develop and where you can survive strategic closures.

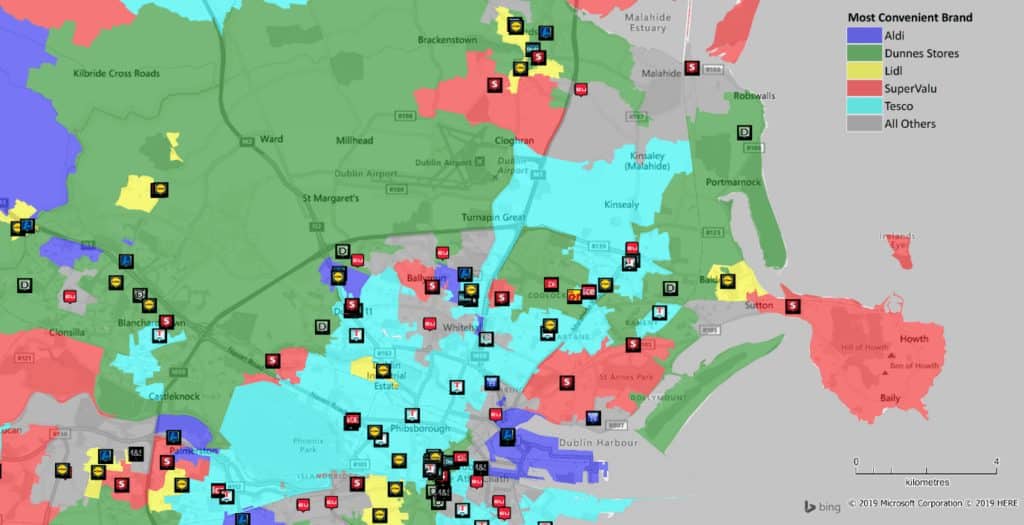

An Irish example: the supermarket convenience model

A recent study carried out by Gamma as part of its Location Insights Series highlights the use of convenience modelling to estimate the relative strength of supermarket retailers. By calculating travel time from every neighbourhood to every supermarket, the study reveals the supermarket grocery brand closest to the most people in the Republic of Ireland.

SuperValu scored the highest, even though it didn’t have the most stores. However, by having a presence in convenient locations, it was closer to more people than its competitors. This shows that volume isn’t everything and the strategic placement of physical stores is what really matters.

Our research also shows that for most FMCG retailers, there is a very strong correlation between a brand’s neighbourhood convenience score and its market share. If you can understand your convenience blind spots and the available market in those locations, you may also understand where you can increase your market share.

The future of store planning

To adjust to the modern retail landscape, most retailers are having to reassess their store estates and design future-proofed networks that combine all channels with the customer at their core. Store location planning now involves designing store networks that better reflect the changing nature of retailing, with ever-evolving ecommerce models offering a multitude of customer interaction points. This makes the process considerably more complicated and now requires a broader and more flexible view of the required retail presence. However, by fully understanding the journey that their customers must take to interact with their brand through omnichannel location analysis, retailers will be able to affect consumer behaviour like never before.

@ 2019 GammaLI.co.uk by Feargal O’Neill

This article first appeared in Checkout Top 100 Brands 2019 (Vol.45 No.8, August 2019).

About the Author

Feargal O’Neill, chief executive officer, Gamma, has over 20 years’ experience in formulating and applying location intelligence strategies in the retail sector. As a location analytics and spatial modelling expert, Feargal helps retailers realise greater benefits from location-based information. Gamma’s Storecast™ platform assists retailers in optimising their store networks for the future.